September Real Estate Report 2023

Real Estate Market Analysis: Current Housing Inventory Trends

The existing housing inventory is a paramount determinant in today's real estate landscape. For potential sellers, this presents a significant advantage. Given the low housing inventory, a strategically priced property will capture market attention and sell quickly.

“Two factors are driving current sales activity – inventory availability and mortgage rates,” said NAR Chief Economist Lawrence Yun. “Unfortunately, both have been unfavorable to buyers.”

Seasonal Trends vs. Current Market Anomalies

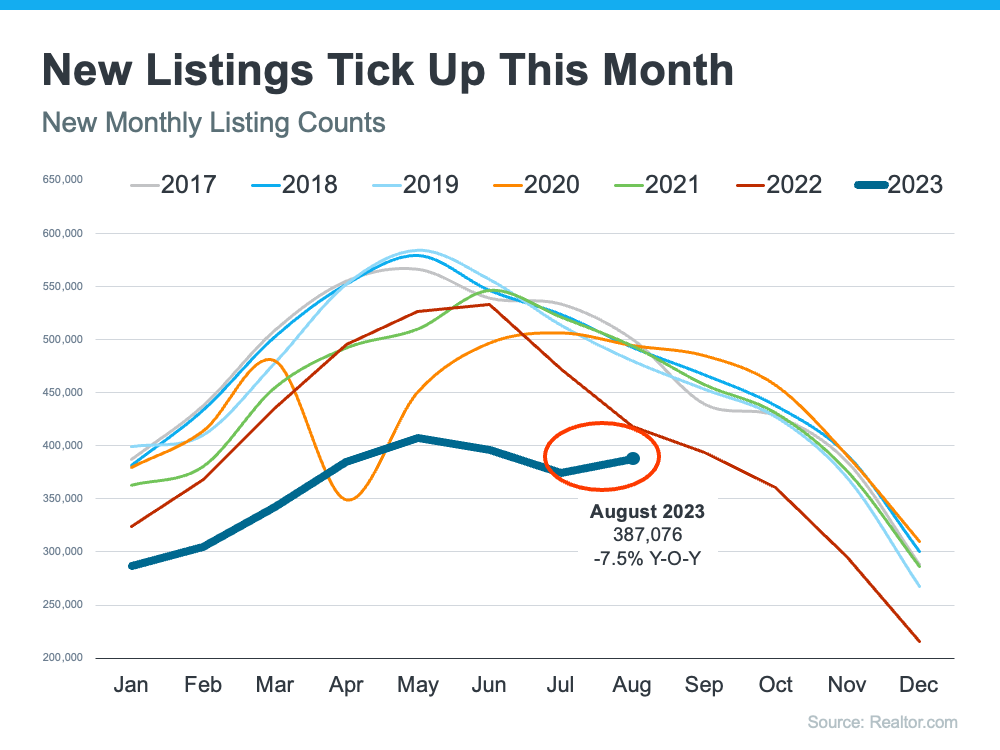

Historically, the real estate market experiences its zenith during the spring buying season. This period witnesses a consistent surge in new listings as sellers strategically position their assets for the active buyer's season. Conversely, market activity traditionally diminishes as the academic calendar resumes and the holidays approach.

Interestingly, recent data from Realtor.com shows an anomaly. There is a discernible increase in property listings later in August than typically observed. Such a deviation from established market patterns is consequential. This is unusual generally; the opposite is true between July and August.

The inventory of unsold existing homes increased by 3.7% from the previous month.

There are enough unsold homes on the market to last 3.3 months at the rate they’re currently being sold. This is more than in June, which had a 3.1-month supply, and more than in July last year, which had a 3.2-month supply.

What we're observing is a shift in sellers' perspectives. It seems they're thinking, "I've been patient enough. I've adjusted to the higher interest rates above 7%. I now realize I could purchase a new home without stressing over a mortgage due to built equity or with a substantial down payment.” Thus, more sellers are entering the market. As both buyers and sellers adjust to this reality of interest rates being over 7%. Cash buyers are becoming more prominent, reinforcing that inventory continues to dominate market dynamics. This generally applies to the baby boomers. It boils down to one apparent factor: they possess substantial property equity.

In July, 26% of the homes were bought using only cash. According to NAR, this is the same as June, but it’s more than July of last year when 24% were all-cash buys.

So, currently, we're seeing homes remaining on the market for extended periods; investors and baby boomers are unphased by market challenges. It's important to note that in a balanced and healthy market, we typically have a six-month supply of inventory; however, we are at 3.3 now, which is still a challenge.

Analyzing Home Equity and Its Implications on Selling Decisions in the Current Market

Our examination of homeowners' positions shows that mortgage percentages significantly influence their decision to sell. Those homeowners falling under the 3% mark are unlikely to consider selling, barring a significant lifestyle shift. Homeowners bracketed between 3% and 4%, and even up to 5%, may also exhibit hesitancy in selling. Contrastingly, homeowners operating between 5% and 6% mortgage rates appear more inclined to sell, undeterred by prevailing rates. Moreover, homeowners with mortgages exceeding 6% are ready to engage with the market.

A pertinent finding from our recent survey highlighted that mortgage rates play a diminished role in selling decisions for older homeowners. Evaluating the data, approximately 26% of US homeowners indicated that elevated mortgage rates would not deter their selling intentions. This translates to one in four homeowners or, for a clearer perspective, two would be undeterred by high mortgage rates in a room with eight homeowners. Delving deeper into the 26% demographic, 43% disclosed they wouldn't require a new mortgage for their subsequent home purchase. This sentiment was profoundly rooted among the baby boomer generation, showcasing heightened confidence primarily from substantial home equity.

The equityy distribution chart reveals compelling insights:

A significant 38.7% represent homeowners who own their homes outright, with no mortgage obligations.

30% of homeowners hold over 50% equity, implying that on a $400,000 property, their equity position exceeds $200,000.

A further 20.8% possess equity ranging between 30% and 50%.

The light blue segment denotes homeowners with 10% to 30% equity.

The orange section marks those with an equity position between zero and 9%.

The minuscule demographic of 0.12% represents homeowners in a negative equity situation.

The data underscores a notable accumulation of home equity, especially among older generations. This equity is a pivotal determinant for homeowners contemplating varying housing needs, whether upsizing, downsizing, or relocating.

“Most homeowners continue to enjoy large wealth gains from recent years with little concern about home price declines,” Yun said. “However, many renters are concerned as they’re facing growing affordability challenges because of high-interest rates.”

Leveraging Home Equity: A Strategic Advantage in Today's Real Estate Market

In the current real estate climate, many prospective buyers and sellers need more confidence in making definitive moves. However, homeowners with significant equity are uniquely positioned to navigate this environment more confidently. This substantial equity affords them distinct advantages over those without such a robust position. Let's delve into the top three benefits they can leverage:

All-Cash Purchase Power: Homeowners with ample equity can transition into all-cash buyers. This liberates them from mortgage payments and renders them highly attractive to sellers. Cash offers often expedite transactions and eliminate the uncertainties associated with mortgage approvals. Such buyers are indifferent primarily to interest rate fluctuations, as monthly mortgages bind them. Moreover, cash transactions can also bolster their negotiation stance, potentially resulting in more favorable purchase terms.

Equity Awareness: A recurring trend observed in numerous surveys is that many homeowners often underestimate the equity they've amassed in their homes. An appreciation of this equity can significantly offset concerns regarding rising mortgage rates. If homeowners opt for an all-cash purchase, they can bypass the effects of these rate hikes altogether. Further, the financial benefits from downsizing or relocating to a region with a lower cost of living can eclipse the incremental charges stemming from elevated mortgage rates.

Strategic Financial Planning: The primary objective is to enlighten these homeowners about their choices, empowering them to make decisions aligned with their present and future requirements. Our role extends beyond mere transaction facilitation; it's about forging lasting relationships, cultivating trust, and ensuring clients are poised to make optimal decisions for their well-being.

In summation, the current market presents challenges and opportunities for those with significant home equity. By recognizing and harnessing their unique advantages, they can make informed decisions that align with their financial goals and lifestyle aspirations.